The headline points for busy readers

In 2016, when the Falkland Islands Government (FIG) was deciding how to structure a new exclusive telecommunications licence for Sure, it did not lack for warnings. Its own consultants had set out a menu of alternatives to straight renegotiation. The Chamber of Commerce, individual residents and even the Select Committee’s own line of questioning raised specific, detailed concerns about the length of exclusivity, the weakness of the terms on offer, and the risk of locking the Islands into a decade-plus arrangement without adequate safeguards. Almost a decade on, many of those warnings read as remarkably accurate predictions of where we’ve ended up. As FIG prepares an August 2026 ExCo paper that will again ask whether to renegotiate continuity with Sure or pursue something different, this post asks a simple question: were the 2016 warnings actually addressed, or is the community being asked to take the same gamble twice? The past can inform the future.

A choice presented as the safe one

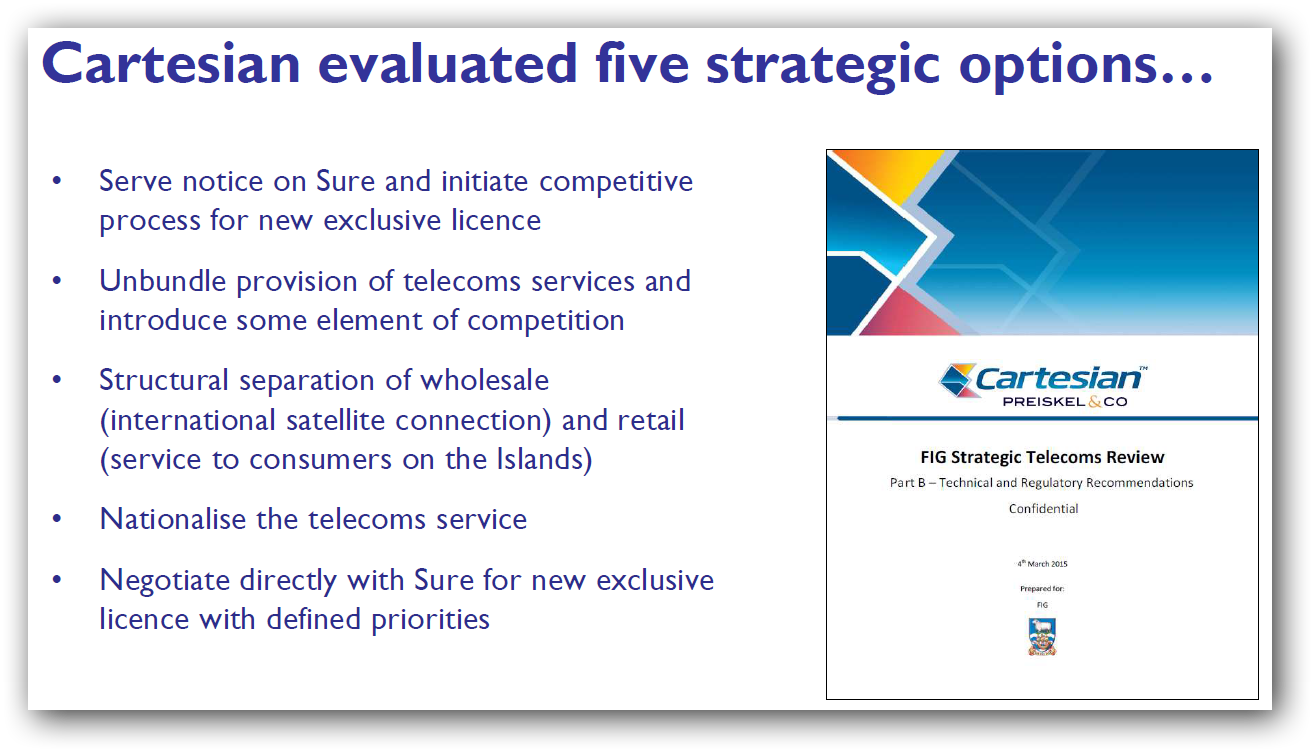

It’s worth remembering that in 2016, renegotiating directly with Sure was never the only option on the table. FIG consultants, Cartesian, working with legal advisers Preiskel & Co, evaluated a full range of alternatives: serving notice and running a competitive process for a new exclusive licence, unbundling services to introduce an element of competition, structurally separating the wholesale satellite link from retail service delivery, taking the network into public ownership, or negotiating a new exclusive agreement with Sure.

Cartesian ultimately recommended negotiation, and the FIG’s own economic analysis reached the same conclusion. The reasoning, set out in the October 2016 Executive Council paper, was that the Islands’ small and dispersed population meant that Stanley, Camp and Mount Pleasant together were unlikely to sustain a competitive market at reasonable prices without government intervention, and that regulating a genuinely competitive market would itself exceed the Government’s practical capacity. On its own terms, that reasoning was defensible, and this post is not arguing that exclusivity should necessarily have been rejected altogether.

What is often forgotten, however, is that Cartesian’s recommendation was explicitly conditional. At the public meeting held on 16 November 2016 – held 19 months after ExCo approved an exclusive licence with Sure – officials explained that the final Cartesian reports had been received in March 2015 and that the Executive Council had agreed the following month to begin commercial discussions with Sure. The consultants’ recommendation was to “negotiate directly with Sure for a new exclusive licence with defined priorities”, with the Government’s economic analysis aligning with that recommendation. Crucially, however, the presentation also made clear that a competitive tender or an unbundled model remained available if acceptable terms could not be reached through negotiation.

In other words, negotiation was never intended to be an end in itself. It was one strategic option, supported by a credible fallback if negotiations failed to secure an acceptable outcome. As events unfolded, that fallback was never invoked.

The concerns raised at the time

The November 2016 Select Committee, held 19 months after ExCo’s decision, scrutinising the Communications Bill, heard sustained, specific objections rather than vague unease. The Chamber of Commerce, represented by Executive Secretary Stacy Bragger (a current MLA), told the Committee it had been raising concerns with FIG since 2013 through position papers, presentations to the Telecommunications Working Group, and repeated letters, and said it was left deeply disappointed by where the Bill and licence had ended up.

Written submissions to the Committee went into greater detail. One submission questioned why the exclusive agreement appeared to value the exclusive licence at only £10,000 when the incumbent’s recorded profit the previous year had been over five million pounds. Another submission, from resident Drew Irvine, argued that the returns being made by a monopoly provider were already excessive, that self-provision and genuine competition were the only real check on price and quality, that the accounting behind the licence lacked transparency, and that placing heavy faith in a Regulator and Regulations was hard to justify given the arrangement’s track record over the previous two decades.

None of this was abstract muttering from the sidelines. It was detailed, repeated, on the record, and delivered directly to the people who would go on to approve the Bill and the licence.

What was recommended, and what was actually signed

Perhaps the clearest sign that these warnings had some substance is that even Cartesian’s own confidential recommendations were more cautious than what FIG ultimately agreed. Cartesian’s Part B advice proposed a licence with an initial term of ten years and a notice period of three years within that first decade, tightening to two years after that. What FIG actually signed with Sure in April 2017 was a licence backdated to run from January 2016, for an initial term of twelve years, a structure that sits uneasily against the three licence models the FIG’s own Communications Ordinance was simultaneously being drafted to allow.

The 2016 ExCo paper had also pointed to detailed exit provisions, covering the handover and compensation at the end of a licence, as one of the clear improvements the new regime would deliver over the old arrangement, which officials said had left FIG open to being held to ransom by the existing provider. Those exit provisions are precisely the section of the signed licence that remains blacked out in the public copy today.

The Community Was Not Consulted — and Said So

It is worth recalling that when the Communications Bill was passing through the Legislative Assembly in 2016, the community raised serious concerns about the lack of meaningful consultation with islanders. At the belated Select Committee on the Communications Bill, held in November and December 2016, multiple witnesses called for a delay to allow proper public consultation before the Bill was passed. The Chamber of Commerce went further, arguing that the entire process should start again with a proper tender exercise and genuine community engagement before any decision was made.

FIG proceeded anyway. The Bill was passed, the licence was signed, and the community’s call for meaningful consultation before a ten-year commitment was not heeded. A decade later, the community finds itself in exactly the position those witnesses warned about: locked into an arrangement that is proving difficult and costly to change, with limited public visibility of the reasoning behind the decisions that created it.

Did the 2016 warnings come true?

Looking at where things stand now in 2026, it’s hard to argue that the Chamber and Mr Irvine were wrong to worry. The Public Accounts Committee’s 2025 review of over £8 million paid or committed to Sure since 2018 concluded it would be very difficult to demonstrate value for money from that spending. Sure’s Falklands operation has reportedly returned a net margin of around 29 per cent, with dividends of roughly £8.5 million in 2022 and £9 million in 2023 flowing to its parent company, paid in the same years FIG was subsidising the company’s satellite capacity by over £1 million annually. The narrow, personal-use only model that now governs how businesses can use Starlink traces directly back to the broad definition of exclusivity in the 2017 licence, years before Starlink was even a realistic option.

In other words, the concerns raised at the Select Committee in 2016, about excessive profitability, weak transparency, and a Regulator being asked to do more than it could realistically deliver, were not idle. They described, with reasonable accuracy, the decade that followed.

Some lessons from 2016 for 2026

If many of the concerns raised in 2016 can now be tested against a decade of experience, the obvious question is what should be done differently as the Falklands Government prepares its decisions for August 2026. The historical record points to several practical lessons that, amongst others, deserve careful consideration before any new long-term agreement is reached.

- Openly weigh all the options, not just a continuity route. The August ExCo paper faces broadly the same menu of Cartesian set out in 2016: tender the licence, unbundle services, separate wholesale from retail, take the network into public ownership, or negotiate a new Sure continuity deal. In 2016, that menu was presented, but the negotiated continuity route was reached quickly and matched FIG’s own starting preference. This time, the alternatives deserve genuine, visible consideration on their own merits, rather than being treated as a mere formality on the way to a foregone conclusion.

- Let community scrutiny happen BEFORE terms are locked in, not after. The Chamber of Commerce and residents raised detailed concerns in the belated 2016 Select Committee, and the Bill proceeded largely unchanged anyway. A Select Committee process this time should let any concerns really shape the outcome, not just be noted and ignored. Papers should be published with appropriate redactions if necessary for discussion, not just withheld for “commercial confidentiality” reasons.

- Make transparency a licence condition. There was no obligation on Sure to publish the financial details needed to judge whether the public is getting value for money. Any new agreement should require regular, public financial reporting as a term of the licence itself, not something FIG has to negotiate for after the fact.

- Build in a review point, not just a distant exit. The 2017 licence has no mechanism to revisit terms if circumstances change materially, and Starlink’s arrival was exactly that kind of change. A new agreement needs a genuine mid-term checkpoint, not just one notice window years away.

- Define exclusivity narrowly, with future technologies in mind. The current ban on business use of Starlink exists only because “commercial telephony satellite services” was defined broadly in 2016, years before Starlink existed. Any new scope should be tight enough not to foreclose options nobody can yet anticipate.

- Carve out room for major strategic developments in advance. Premier Oil warned in 2016 that an exclusive licence could inadvertently block it from sourcing its own communications for the Sea Lion development. That concern is far more live now than it was then, and any new licence should explicitly reserve space for large industrial or economic developments to arrange their own solutions.

- Don’t let the most important section be the redacted one. The 2016 ExCo paper cited detailed exit and compensation provisions as proof that the new regime had fixed the “held to ransom” problem. Redacting that same section in the final licence rendered the point moot. Exit terms should be open to public scrutiny.

- Treat the fallback option as real, not as cover. Cartesian’s plan kept open the option to tender or unbundle the licence if talks with Sure failed. There’s little sign that leverage was ever seriously used. A credible alternative only means something if FIG is genuinely prepared to walk toward it.

The same questions, again, in August 2026

FIG is now preparing to decide whether, and when, to serve notice on Sure. The shape of the options is strikingly familiar to 2016: a small, dispersed population; a consultant’s report weighing the same broad set of options; and an incumbent whose cooperation FIG will feel it needs to secure a stable transition.

What should be different this time is that FIG can no longer claim the risks are theoretical. In 2016, the Chamber of Commerce and individual residents were making predictions. By 2026, those predictions can be tested against a decade of evidence from the Falkland Islands itself: PAC findings, public subsidy payments, the Starlink compensation agreement, and Sure’s continuing profitability all provide a factual record against which the decisions of 2016 can now be judged.

The Cartesian review also provides an important reminder. Its recommendation to negotiate with Sure was conditional on acceptable terms, not an endorsement of negotiation at any cost.

If the August 2026 ExCo paper again favours a negotiated extended licence arrangement with Sure, the community should be asking whether that choice is reasonable in principle; given the Islands’ size, it may well be. The more important question is whether the eight lessons identified above will genuinely shape the approach taken this time, or whether the concerns raised in 2016 have once again been acknowledged without fundamentally changing the outcome.

The Connected Falklands Group’s current call for a Select Committee on the post-2027 framework is not a new idea. Similar calls for greater public scrutiny and engagement were made in 2016. The August decisions will show whether the FIG has chosen a more open approach to telecommunications decision-making than it did a decade ago.

Chris Gare, OpenFalklands, July 2026, copyright OpenFalklands

It’s interesting to see how these early decisions around infrastructure can still have implications down the line, especially with future technology developments.